Field note · June 26, 2025

Who Really Drove Hybrid-Casual?

A client asked: "Who have been the big players most responsible for hybrid casual?"

I realized I didn't have as crisp a mental image as I should.

I knew Voodoo, Rollic, Homa were in the picture, but was less clear on which games, and at what scale / timeframe.

SO, for anyone in similar straits

Who has really been driving Hybrid-Casual's ascent?

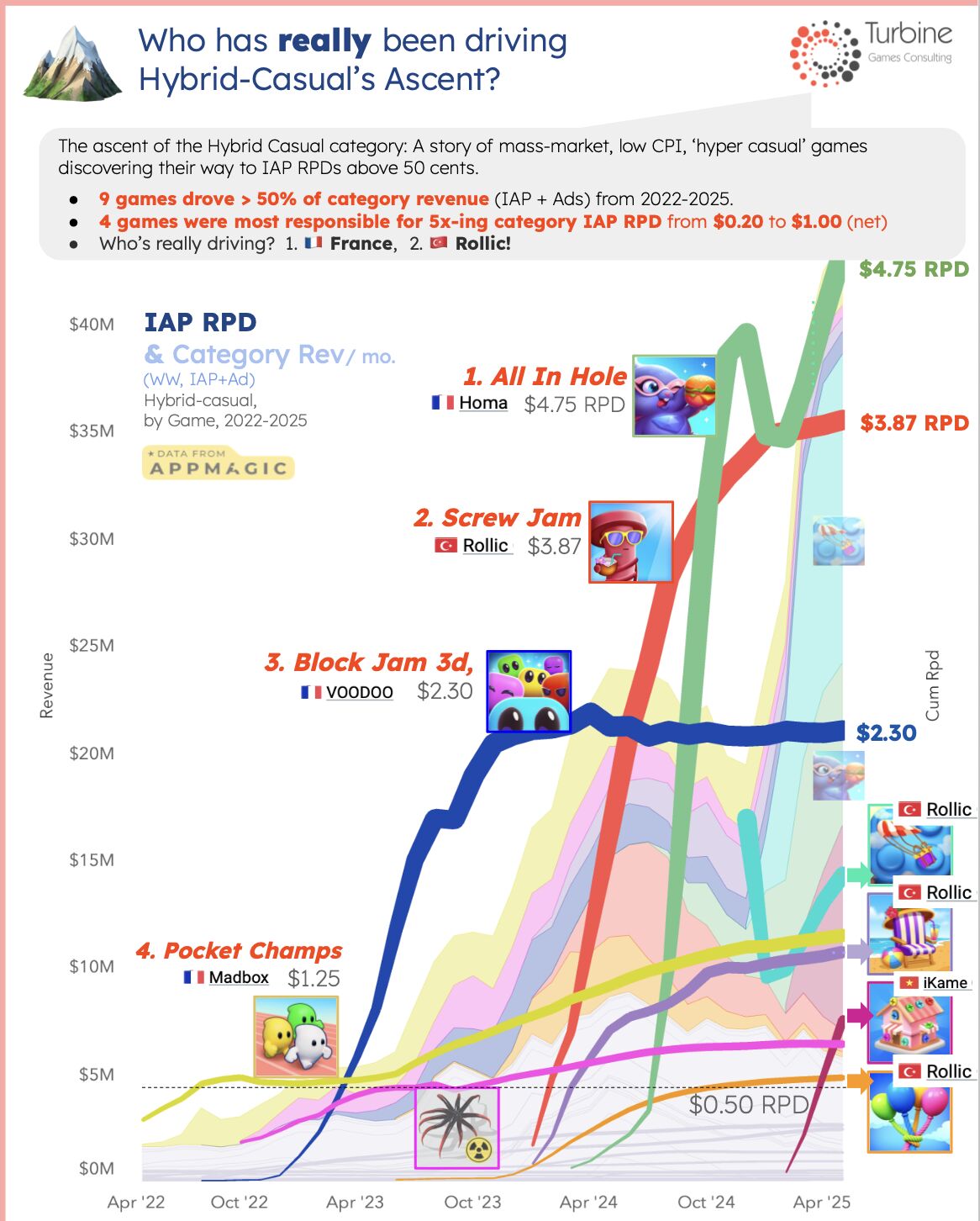

- The French Triad (Homa, Voodoo, Madbox: 43% of Rev since '22)

- Rollic (26%)

- Everyone else? 31%

So 69% of Hybrid-Casual Revenue (IAP + Ads) has been driven by 3 French Publishers, and Rollic (Turkey).

Since IDFA Deprecation (2021), the big beats IMO

- Jun '23: Block Jam 3D (Voodoo) is first Hybrid title to reach $2 RPDs (IAP+Ads)

- Apr '24: Screw Jam (Rollic) is first to break $3.

- Aug '24: All In Hole (Homa) is first to break $4.

- Dec '25: Color Block Jam (Rollic) launches with $1.50 RPDs, but scales really aggressively to dominate category revshare.

Overall, the ascent of Hybrid Casual is the story of mass-market, low-CPI 'hyper casual' puzzle games discovering their way to IAP RPDs above 50 cents.

This includes, in no small part, learning to embrace the ubiquitous loss-aversion and live-ops mechanics of the casual match-3 genre..

Most copied exemplar (unsurprisingly): Royal Match.

Does this capture the full story? Anyone I missed?

PS: This analysis excludes 'Hybrid-Midcore' titles (e.g. Habby).

(Data from AppMagic's Market Segment Tool)

Turbine helps mobile game & app publishers drive UA and product KPIs.

Book Intro Call View original on LinkedIn →